Investors looking for a reliable, inflation‑hedging cash flow often ask how to buy commercial real estate for long‑term income strategy; the answer is to focus on properties with strong tenant demand, stable cap rates, and a clear path to value‑add improvements. By targeting assets that generate consistent commercial property cash flow and aligning them with a diversified real‑estate portfolio, you can secure passive income that outpaces most equity markets. For a deeper dive into structuring such investments, see our Real Estate Market Investment Guide for Long‑Term Wealth.

Why Commercial Real Estate Remains a Top Long‑Term Income Engine

In 2026, commercial real estate (CRE) continues to outperform many traditional asset classes because it offers:

- Predictable cash flow: Lease agreements for office, industrial, and retail spaces typically span three to ten years, providing a steady stream of rent.

- Inflation protection: Rental escalations and triple‑net leases shift many operating cost increases to tenants.

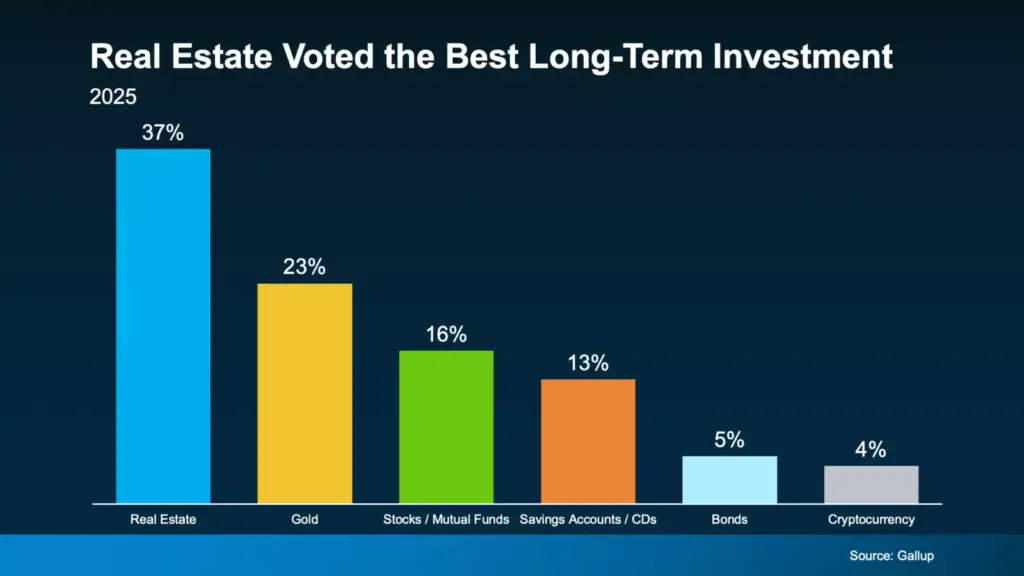

- Portfolio diversification: Adding CRE to a stock‑heavy portfolio reduces overall volatility, as highlighted in a 2025 NCREIF survey.

- Tax advantages: Depreciation, 1031 exchanges, and interest deductions can significantly boost after‑tax returns.

According to CBRE’s Global Real Estate Market Outlook 2026, cap rate compression in prime markets has stabilized around 5.2% for office assets and 4.8% for industrial, signaling investor confidence.

Table of Contents

- Why Commercial Real Estate Remains a Top Long‑Term Income Engine

- Key Metrics to Evaluate Before You Buy

- Capitalization Rate (Cap Rate)

- Cash‑on‑Cash Return

- Occupancy & Tenant Quality

- Debt Service Coverage Ratio (DSCR)

- Step‑by‑Step Blueprint for Acquiring an Income‑Generating Property

- Common Pitfalls and How to Avoid Them

- Real‑World Case Study: A Mid‑Size Office Building in Austin, Texas

- Frequently Asked Questions

- Can I start with a small commercial property?

- How does a 1031 exchange help my long‑term strategy?

- What’s the ideal debt structure?

- Is it worth investing in secondary markets?

- How important is tenant retention?

Key Metrics to Evaluate Before You Buy

Understanding the numbers behind a property is essential for a sustainable income strategy. Below are the most critical metrics for 2026:

Capitalization Rate (Cap Rate)

The cap rate measures net operating income (NOI) relative to purchase price. A lower cap rate indicates higher valuation but often reflects superior location and tenant quality. In 2026, top‑tier urban assets trade at 4.5%‑5.5% cap, while secondary markets hover between 6%‑7%.

Cash‑on‑Cash Return

This metric compares the annual pre‑tax cash flow to the actual cash invested. For long‑term income, investors typically target a cash‑on‑cash return of 8%‑10% after accounting for financing costs.

Occupancy & Tenant Quality

High occupancy (>90%) coupled with credit‑worthy tenants (e.g., Fortune 500 firms, government agencies) reduces vacancy risk. Look for lease structures that include rent escalations and expense pass‑throughs.

Debt Service Coverage Ratio (DSCR)

Lenders require a DSCR of at least 1.25, meaning the property’s NOI should be 25% higher than its annual debt service. A healthy DSCR protects you from cash‑flow shortfalls during economic downturns.

Step‑by‑Step Blueprint for Acquiring an Income‑Generating Property

- Define Your Investment Thesis: Decide whether you aim for value‑add (renovations, lease upgrades) or core (stable, fully leased) assets. This shapes your location and asset‑type criteria.

- Conduct Market Research: Use tools like CoStar, REIS, and the Invest in Florida Real Estate Market 2026 guide to identify sub‑markets with strong job growth and low vacancy.

- Run a Preliminary Financial Model: Input expected rent, operating expenses, financing terms, and projected cap rate to estimate cash‑on‑cash return.

- Secure a Certified Real Estate Lawyer: Legal due diligence—title search, zoning compliance, and lease audits—requires expertise. Learn why a certified lawyer is non‑negotiable in our article Why a Certified Real Estate Lawyer Is Non‑Negotiable.

- Arrange Financing: Compare conventional bank loans, CMBS, and private equity sources. Aim for a loan‑to‑value (LTV) ratio that keeps DSCR above 1.3.

- Perform Property Inspection: Hire a qualified engineer to assess structural integrity, environmental concerns, and any deferred maintenance that could affect cash flow.

- Negotiate Purchase Terms: Leverage findings from inspection and market comps to negotiate price, seller concessions, and lease‑back arrangements if needed.

- Close the Deal: Finalize financing, execute the purchase agreement, and record the deed. Immediately set up an escrow account for operating reserves.

- Implement Asset Management Plan: Optimize rent collections, enforce lease terms, and pursue tenant retention strategies such as lease renewal incentives.

Common Pitfalls and How to Avoid Them

- Overpaying on Cap Rate: Chasing prestige locations without analyzing NOI can erode returns. Stick to a disciplined cap‑rate threshold based on your risk tolerance.

- Ignoring Tenant Mix: Concentrating on a single industry can expose you to sector‑specific downturns. Diversify across retail, office, and industrial tenants.

- Underestimating Operating Expenses: Maintenance, property taxes, and insurance can climb faster than anticipated. Include a 3%‑5% annual expense growth factor in your model.

- Insufficient Due Diligence on Zoning: A property slated for redevelopment may face restrictive zoning. Verify permissible uses before committing.

- Neglecting Professional Management: Self‑managing can lead to missed rent payments and higher vacancy. Consider a reputable property management firm with a track record in your asset class.

Real‑World Case Study: A Mid‑Size Office Building in Austin, Texas

In early 2025, an investor group acquired a 45,000‑sq‑ft office building in Austin’s East‑Side Tech Corridor for $7.2 million. Key highlights:

- Cap Rate at Purchase: 5.6% (NOI $403,200)

- Tenant Profile: 70% occupied by software startups, 20% by a regional university research lab, 10% vacant.

- Value‑Add Strategy: Implemented a $350,000 interior renovation, upgraded HVAC, and added coworking spaces.

- Result After 18 Months: Occupancy rose to 96%, average rent escalated 8%, and the new cap rate settled at 5.2% while cash‑on‑cash return climbed to 9.4%.

The case demonstrates how targeted improvements and tenant diversification can boost long‑term cash flow without over‑leveraging the asset.

Frequently Asked Questions

Can I start with a small commercial property?

Yes. Duplexes, small retail strips, and single‑tenant industrial units often require lower capital outlays while still delivering solid cash flow.

How does a 1031 exchange help my long‑term strategy?

A 1031 exchange allows you to defer capital gains taxes when you sell one investment property and reinvest the proceeds into a like‑kind property, preserving more equity for growth.

What’s the ideal debt structure?

Fixed‑rate loans with 5‑7 year amortizations and an LTV of 65%‑75% typically balance risk and cash‑flow stability, keeping DSCR comfortably above 1.3.

Is it worth investing in secondary markets?

Secondary markets often offer higher cap rates (6%‑8%) and lower entry prices, making them attractive for income‑focused investors seeking yield over prestige.

How important is tenant retention?

High tenant retention reduces turnover costs and vacancy periods. Offering lease‑renewal incentives and maintaining property quality are proven tenant retention strategies.

By adhering to a disciplined acquisition process, monitoring key performance indicators, and partnering with seasoned professionals, buying commercial real estate can become a cornerstone of a long‑term income strategy that delivers both stability and growth.